Book Your Appointment Today!

Our staff will reach out to you shortly

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

When a tooth starts throbbing or you know you’re long overdue for a cleaning, the first thought that often follows is, "How am I going to pay for this without insurance?" It's a stressful feeling, but you’re definitely not alone. The reality is, a huge number of Americans are in the same boat.

It’s estimated that by 2026, around 27% of adults in the U.S.—that’s about 72 million people—won't have any dental insurance. People without dental benefits are actually three times more likely to be uninsured compared to those without general health insurance.

Here in Humble and the greater Houston area, we see this firsthand. Data shows that 36% of uninsured adults skip necessary dental work because of the cost. Unfortunately, this often lets a minor issue, like a small cavity, spiral into a much bigger, more expensive problem down the road.

Instead of letting financial worry take over, the most effective step is to get a clear diagnosis of what's happening in your mouth and learn about the real, practical solutions available to you.

Before you can find the right affordable option, you need to know exactly what you’re dealing with. Is this an urgent problem, or something that's been on your to-do list for a while? Taking a moment for an honest self-check helps you focus your search and explain your situation clearly to a dental team.

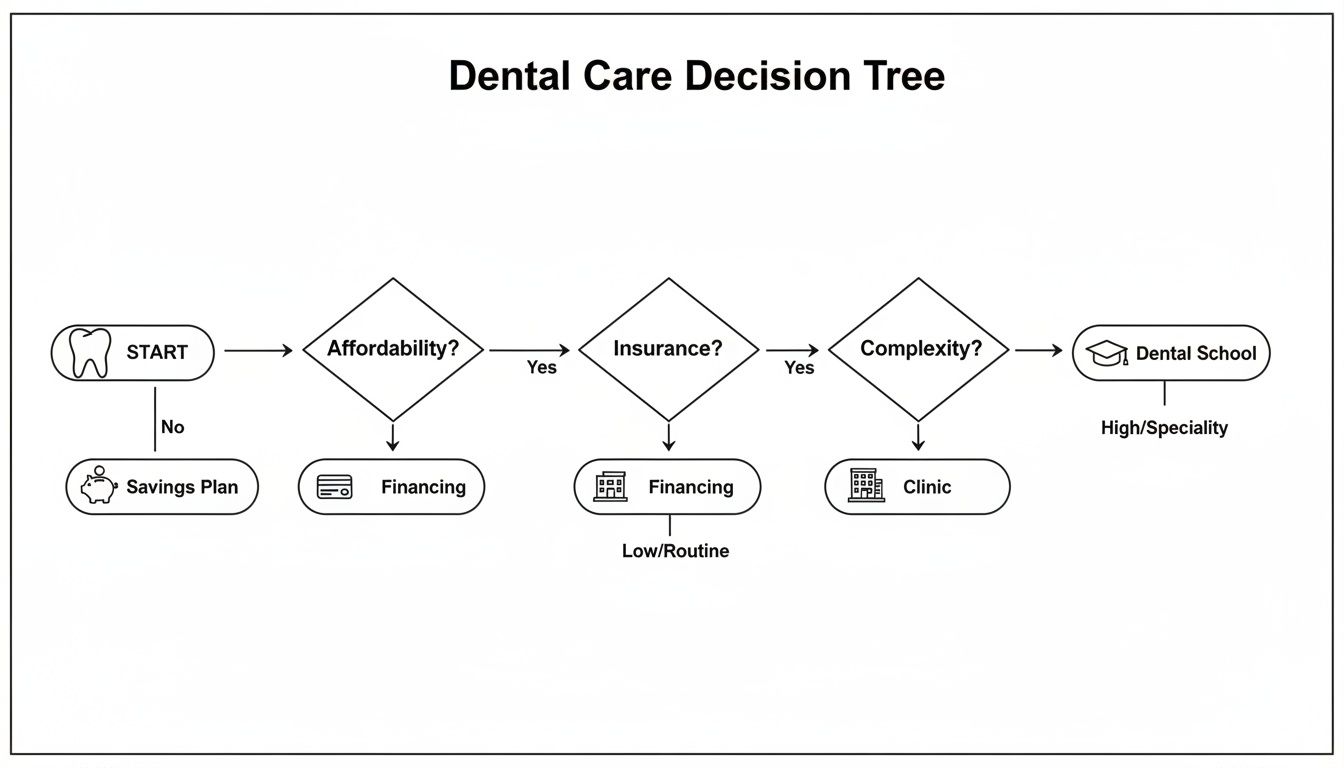

This decision tree gives you a visual map of the different routes you can take to get the dental work you need, even without insurance.

As you can see, no matter where you're starting from—whether you're in pain or just trying to get ahead of problems—there’s a clear, manageable path forward.

Here’s a quick comparison of the most effective ways to access affordable dental care when you don't have traditional insurance coverage.

| Option | Best For | Typical Savings | Key Benefit |

|---|---|---|---|

| In-House Membership Plan | Individuals & families needing regular preventive care (cleanings, exams) and discounts on other treatments. | 20-50% off standard fees. | Predictable costs and immediate access to benefits with no waiting periods or yearly maximums. |

| Third-Party Financing | Major, unexpected procedures like root canals, crowns, or implants that you need to pay for over time. | N/A (focus is on payment plans). | Allows you to get necessary care now and pay for it in manageable monthly installments, often with 0% interest promotional periods. |

| Community & Charity Clinics | Low-income individuals and families needing basic, urgent, or restorative care at a reduced cost. | Varies greatly, often sliding-scale based on income. | Provides a safety net for essential dental services when other options are out of reach. |

| Dental Schools | Patients who need complex work (implants, dentures, crowns) and have the time for longer appointments. | 50% or more compared to private practice fees. | High-quality care from supervised students using the latest techniques, but requires more time and flexibility. |

Each of these pathways offers a solution. The key is to match the right one to your specific dental needs and financial situation.

Once you know what kind of care you need, you can confidently explore these options. Each one is designed for different circumstances, whether you're trying to manage routine costs or figure out how to pay for a big, unexpected procedure.

The most important thing to remember is that you have more power than you think. Delaying care is almost guaranteed to lead to higher costs and more invasive treatments later. Taking a proactive step today can save you a world of pain and money.

Think about it: a small filling might cost a few hundred dollars. If you ignore it, that same cavity can easily turn into an infection requiring a root canal and crown, which can run into the thousands. By exploring your options now, you can tackle the small problem before it becomes a big one. For more local resources, you can also check out our guide on finding affordable dental care in Houston.

What if you could get all your routine preventive care covered for a single, flat annual fee? And on top of that, get significant discounts on any other treatment you might need—all without the usual headaches of deductibles, waiting periods, claim forms, or annual maximums. This isn't some too-good-to-be-true offer; it’s exactly how an in-house dental savings plan works.

These membership programs, offered directly by dental practices like ours, are one of the most straightforward ways to get dental work without insurance. They're designed to make your care predictable and affordable, giving you every reason to stay on top of your oral health.

Think of it less like insurance and more like a membership to a wholesale club, but for your teeth. You pay one annual fee directly to the dental office. In return, you get a whole package of preventive services for the year at no extra cost, plus a set percentage off all other procedures.

Here at Clayton Dental Studio, for example, our Humble Savings Plan does just that. A patient who joins gets all their routine care covered and receives discounts on everything else. It completely changes the game, turning dental budgeting from a source of stress into a simple, fixed cost.

This approach cuts out all the complexity of traditional insurance. You don't have to deal with confusing reimbursement paperwork or cross your fingers hoping a procedure gets approved. The savings are clear and you get them right away.

Let’s look at a common situation. Say a new patient, we'll call her Maria, joins an in-house plan for an annual fee of about $350. The moment she signs up, her membership includes:

If she were paying for those preventive services one by one, the total would easily surpass the cost of the membership. Right off the bat, she’s saving money just by keeping up with her check-ups.

Then, a few months down the road, she chips a molar. We find she needs a crown, which normally costs around $1,500. As a plan member, she gets a 20% discount on restorative work. That saves her $300 instantly, bringing her cost for the crown down to $1,200.

By the end of the year, her savings plan has easily paid for itself and then some. More importantly, it allowed her to get the care she needed—both preventive and restorative—without hesitating over the cost.

While both are meant to lower your costs, their entire approach is different. Knowing these differences is critical if you’re trying to figure out how to get dental work without insurance.

A dental savings plan is built on simplicity and transparency. It removes the "middleman," allowing for a direct financial relationship between you and your dental provider that prioritizes your health, not administrative hurdles.

Here’s a quick breakdown of how they stack up:

| Feature | In-House Savings Plan | Traditional Dental Insurance |

|---|---|---|

| Annual Maximum | None. There's no cap on how much you can save. | Typically capped at $1,000-$2,000 per year. |

| Waiting Period | None. Benefits start the day you sign up. | Often has waiting periods of 6-12 months for major work. |

| Deductibles | None. You never have to pay a deductible. | Requires you to pay a set amount before coverage kicks in. |

| Claim Forms | None. All discounts are applied instantly at the office. | Requires claims to be filed and processed for reimbursement. |

| Pre-Approvals | None. You and your dentist decide on the best treatment. | May require pre-authorization for certain procedures. |

The biggest advantage of a savings plan is freedom. You’re not boxed in by an annual maximum if you happen to need a lot of work, and you never have to put off treatment because of a waiting period. That’s a huge relief, especially if you need care right now.

Of course, not all in-house plans are the same. When you call a dental office to ask about their membership program, having a few key questions ready will help you make sure it's the right fit.

Here's a practical checklist of what to ask:

A reputable plan will have clear, immediate answers for you. It should make budgeting for your dental care feel simple and empowering, finally removing those financial walls that keep so many people from getting the care they deserve.

An in-office savings plan is a fantastic tool for handling routine cleanings and checkups. But what happens when you’re facing something bigger, like a necessary crown or a dental implant? These treatments are absolutely critical for restoring your bite and preventing a cascade of other oral health issues, but the price tag can feel overwhelming.

This is exactly where dental financing comes into play. Think of it as a bridge that gets you the care you need now, with a plan to pay for it over time.

These options function a lot like specialized healthcare credit cards. They close the gap between the upfront cost of treatment and what you can comfortably pay out-of-pocket. This is so important, because delaying care almost always leads to more extensive and expensive problems. For instance, putting off a crown can cause the tooth to fracture so badly that it can no longer be saved, turning a straightforward fix into a complex extraction and replacement.

Many dental practices, including ours, partner with third-party financing companies to make care more accessible. You’ll often see well-known names like CareCredit and Cherry. These services are designed specifically for healthcare costs, allowing you to break a large bill into manageable monthly payments.

The application process is refreshingly simple. You can usually apply from home or right in the office and get a decision in just a few minutes. That immediate answer means you can move forward with your treatment plan right away.

The real game-changer to look for is an interest-free promotional period.

It’s the best of both worlds. You get the treatment you need immediately, but you can spread the cost out over months without paying a penny extra in interest.

Let’s say you need a same-day crown that costs $1,500. You don't have that sitting in the bank, but you know the tooth can’t wait. Our office helps you get set up with a 12-month, interest-free financing plan.

After a quick application, you’re approved. Instead of a single, stressful payment, your financial picture now looks like this:

Suddenly, that essential crown feels completely achievable. A $125 monthly payment fits into a budget far more easily than a $1,500 lump sum, allowing you to prioritize your oral health without derailing your finances.

The entire point of financing is to empower you to say “yes” to the best treatment for your long-term health. It transforms a large, intimidating number into a simple, predictable monthly expense.

Applying for these plans is usually straightforward, and a good dental team will walk you through it. A little preparation on your end can make the process even smoother.

1. Know Your Credit Score

Approval is often based on your credit history. Checking your score beforehand using a free service like Credit Karma gives you a good idea of what to expect.

2. Have Your Information Ready

Applications require standard personal details, your social security number, and an estimate of your annual income. Having this information handy will speed up the process.

3. Ask About All Available Plans

A dental office might work with more than one company or offer several different payment terms. Be sure to ask about all your options so you can pick the plan with the monthly payment and timeline that works best for you. Learning the ins and outs of both dental in-house financing and third-party plans will help you make a confident decision.

By using these financing tools wisely, you can get any dental work you need without insurance—ensuring even major procedures like implants and crowns are well within your reach.

When you're facing a dental problem without insurance, a key question is, "Where do I even start?" The good news is, for residents in Humble and the greater Houston area, there are several community and public health resources designed specifically to bridge this gap.

Navigating these options is a little different than a typical private practice visit, but they provide a crucial safety net. Here is a practical guide to the best avenues—community clinics, dental schools, and charity programs—so you can find the right fit for your needs and budget.

For many people without insurance, community dental clinics are the most direct path to affordable care. These are often called Federally Qualified Health Centers (FQHCs), and their entire mission is to provide healthcare, including dentistry, to the community regardless of someone’s ability to pay.

These clinics almost always operate on a sliding-scale fee model. This is a game-changer. It means what you pay is calculated based on your income and household size, making essential care accessible even on a very tight budget.

What you need to know:

If you need more complex work done—think root canals, crowns, or dentures—dental schools are an incredible resource. Houston is home to excellent dental programs where students, under the constant and strict supervision of licensed, veteran dentists, provide high-quality care.

Every step is performed by a dental student but checked and approved by an experienced professor. This meticulous process ensures fantastic quality but also means your appointments will be much longer than at a private practice.

Dental schools are a win-win: patients receive top-notch, affordable care for complex issues, and the next generation of dentists gets invaluable hands-on experience. The savings can be substantial, often 50% or more compared to private practice fees.

This makes dental schools a phenomenal choice when you have some flexibility in your schedule but need major work done without the major price tag.

A sudden, throbbing toothache or a knocked-out tooth doesn't give you the luxury of waiting weeks for an appointment. You need pain relief and treatment now. For a complete breakdown, check out our guide on what constitutes a dental emergency and how to handle it.

Here's your immediate action plan:

Virtual care is also changing how we handle these situations. Teledentistry is projected to handle 30% of all dental consultations by 2026. With 30-50% of dental issues going untreated in countries like the U.S., a hybrid approach can be a lifesaver. You could start with a quick virtual chat to diagnose the problem, then come in for the hands-on treatment you need. It's an efficient way to get help fast.

While we’ve covered many ways to find affordable care when you need it, the single most powerful tool for managing costs is prevention. It's about shifting your mindset from putting out fires to stopping them before they start. This is your best defense for protecting both your smile and your wallet.

Honestly, the cheapest dental work is the work you never have to get done. Adopting this mindset is crucial when you're navigating care without traditional insurance.

I get it. When you're watching every dollar, a professional cleaning can feel like an optional expense. But from a dentist's perspective, skipping cleanings is one of the costliest long-term mistakes a patient can make.

No matter how well you brush and floss, you cannot remove tartar (hardened plaque) on your own. Only a dental hygienist's tools can. If left to build up, tartar is a direct cause of cavities and gum disease.

Think of it like an oil change for your car; you spend a little now to avoid catastrophic engine failure later. Regular cleanings are a smart investment. An in-house membership like our Humble Savings Plan often covers these visits completely, making it a sound financial decision.

Let's look at real numbers. Say we catch a small cavity during a check-up. The fix is a simple filling, which might cost a few hundred dollars out-of-pocket. It’s manageable.

But what happens if you skip that visit? The cavity grows, burrowing deeper until it reaches the nerve inside your tooth. Suddenly, you're in severe pain. That "small problem" is now an infection requiring a root canal and crown, a procedure that can easily run $2,000 to $3,000 or more.

A small, treatable issue can explode into a major financial headache just by waiting. Proactive care isn’t just good for your health; it's financial self-defense.

Your body is pretty good at telling you when something’s not right. The trick is learning to listen. Tuning into these early signals gives you the power to act before a tiny issue becomes a big one.

Keep an eye out for these subtle clues:

If you notice any of these, don't just hope it goes away. A quick consultation can pinpoint the problem while it’s still simple and inexpensive to fix.

It’s no secret that what you eat directly impacts your teeth. Sugary and acidic drinks—soda, sports drinks, even some fruit juices—are a major culprit. They attack your tooth enamel, leaving it vulnerable to decay. Making simple swaps, like choosing water over soda, is a free and effective way to protect your smile.

In the office, we also have amazing technology on our side. At Clayton Dental Studio, for example, we use AI-powered X-rays to see things the human eye can't. This tech helps us spot decay in its infancy, sometimes before it's even visible. Catching problems this early means treatments are quicker, less invasive, and much more affordable. It puts you back in the driver's seat of your dental and financial health.

When you don't have dental insurance, every little twinge in your tooth can feel like a countdown to a financial headache. It's completely normal to have questions, even after you’ve researched your options. We hear them every day from patients in our community.

Let's clear the air and tackle some of the most common questions with direct, actionable answers. Our goal is to give you the confidence you need to move forward and get the care you deserve.

Yes, you absolutely can, and you should. Think of it less as a hard-nosed negotiation and more as a collaborative conversation. Most private dental practices genuinely want to find a way to make your treatment possible.

A great starting point is simply asking if there are different treatment options available at different price points. For instance, in some cases, a dental bridge might be a more budget-friendly path forward compared to a dental implant.

Here are a few specific things you can bring up:

It truly never hurts to ask. A good dental team would much rather find a solution that works for you than see you put off necessary care.

For many people who don't have insurance through an employer, the answer is a definite yes. A dental savings plan is often a much more practical and straightforward choice for managing your oral health.

The big difference is in how they’re built. Dental insurance is a complex system of shared risk, which means you run into deductibles, waiting periods, and annual maximums that can cap your care. A savings plan is built for one thing: simplicity.

A dental savings plan delivers immediate, predictable discounts without all the red tape. It’s designed to make proactive care easier, while traditional insurance often has rules that can unfortunately cause people to delay it.

Just think about it: if you suddenly crack a tooth and need a crown, many insurance plans have a six-month or even a one-year waiting period for major work. With an in-house savings plan, your discount is active the moment you sign up. For everything from routine cleanings to common procedures, a savings plan usually offers more transparency and a better bang for your buck.

A dental emergency is scary enough without worrying about the bill. First things first: if you have severe facial trauma, bleeding that won't stop, or swelling that’s making it hard to breathe, head straight to a hospital emergency room.

For everything else—a severe toothache, a broken tooth, or a lost filling—your first move should be to call local dental offices. Many of us have an emergency number on our after-hours voicemail. When you call, be direct: explain that you're in pain, it’s an emergency, and you're uninsured.

Most dentists are driven by a desire to help get you out of pain. Once you’re in the chair, the team can focus on immediate relief. Then, we can sit down with you to discuss payment options for any follow-up treatment, which almost always includes financing plans. Don't let fear of the cost keep you from calling—an untreated dental infection can quickly become a much more serious medical emergency.

Absolutely. Dental schools are a fantastic and totally safe choice for high-quality, low-cost care, especially for complex procedures like root canals, dentures, or implants.

Every single step of your treatment is performed by a dental student, but they are under the constant, direct supervision of experienced, licensed dentists who are faculty members. The environment is meticulous and follows the strictest, evidence-based protocols with modern equipment.

The only real trade-off is time. Appointments are much longer because a professor has to check and approve every single stage of the work. But the savings are significant—often 50% or less than what you'd pay in a private practice. It's an incredible resource for getting major work done on a tight budget.

At Clayton Dental Studio, we truly believe everyone deserves a healthy, confident smile, no matter their insurance status. From our own in-house Humble Savings Plan to flexible financing, we’re committed to making top-tier dental care accessible for our Humble and Houston neighbors. If you have more questions or you're ready to take the next step, visit us online at claytondentalstudio.com to get started.