Book Your Appointment Today!

Our staff will reach out to you shortly

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Dental in-house financing is a direct payment plan offered by your dentist's office. It’s a practical tool to break down the cost of treatment into manageable installments over time, often with 0% interest. This approach eliminates third-party lenders, making essential dental care more accessible and less stressful. By understanding how it works, you can make informed decisions about your oral health without financial strain.

Imagine you need a dental crown, but the upfront cost is a concern. Instead of navigating the complexities of applying for a new credit card or a bank loan, your dental office offers to split the total cost into smaller, predictable monthly payments. That is the essence of dental in-house financing: a direct financial agreement between you and the dental practice you already know.

This arrangement simplifies the entire process. There are no complex external applications to complete and no lengthy waits for third-party approval. Because it's a direct relationship, the terms are often more flexible. You and the office staff collaborate to create a payment schedule that fits your budget, allowing you to begin treatment without delay.

For many individuals, in-house financing is the key that unlocks necessary dental care. It has become a crucial tool for practices to bridge the gap between the cost of treatment and what patients can realistically afford. To put this in perspective, private insurance in the U.S. covers only about 42% of all dental spending. This leaves many people facing significant out-of-pocket costs, particularly for cosmetic or complex restorative procedures.

By offering these direct payment plans, dental offices help close that financial gap, enabling more patients to say "yes" to the care they need. This model is particularly beneficial for those without insurance or with limited coverage. If this describes your situation, our guide on dentist payment plans without insurance provides additional helpful strategies.

The core principle is straightforward: Good dental health shouldn't be postponed due to financial hurdles. In-house financing removes the immediate cost barrier, empowering you to prioritize your well-being without financial strain.

The primary difference lies in the relationship. With third-party financing, you enter an agreement with a separate financial company. With an in-house plan, you work directly with the team at your dentist's office. This personal connection often leads to distinct advantages:

Think of dental in-house financing not as a formal bank loan, but as a collaborative agreement with your dental office. The process is designed to be transparent and straightforward, allowing you to focus on your health rather than financial complexities.

Here is a practical, step-by-step breakdown of what you can expect. The goal is to keep the process simple and stress-free.

The entire arrangement is typically handled by your dental team, eliminating the need to deal with external websites or wait for third-party approvals.

The Initial Consultation and Treatment Plan: Your journey begins with a dental visit. After an examination, your dentist will outline a clear treatment plan, detailing the required procedures and the total cost. This is your opportunity to ask questions about your dental health and the recommended care.

Discussing Your Payment Options: With the cost established, the office manager or financial coordinator will review payment options with you. They will introduce their in-house financing plan, demonstrating how the total cost can be divided into smaller monthly payments. This is a practical conversation, not a sales pitch.

A Simple Application: The application is typically a short, one-page form. Most dental offices prioritize your ability to make payments over a perfect credit score, so they generally request only basic personal information and potentially proof of income.

Agreeing on the Terms: You and the office team will finalize the details together. This includes the down payment (if any), the precise monthly payment amount, the payment schedule, and the duration of the plan. You will receive a clear, easy-to-understand agreement with no hidden fees.

Real-World Scenario: Let's say you need a root canal and crown that totals $4,000. With an in-house plan, you might put down $400 and then pay the remaining $3,600 in 12 monthly installments of $300—often with 0% interest.

To ensure the arrangement fits your budget and there are no misunderstandings, it is wise to ask specific questions before committing. Being proactive provides clarity and control. For more tips on managing dental costs, our guide on how to afford dental work offers further insights.

Here are four essential questions to ask:

By following these steps and asking the right questions, you can proceed with your dental care feeling confident and in control of your finances.

Navigating how to pay for dental care can feel overwhelming. To provide clarity, let's compare dental in-house financing with other common options, such as third-party lenders and dental savings plans. This will help you identify the most suitable path for your needs.

Think of it this way: an in-house plan is a direct agreement with your dentist. A third-party loan introduces an external financial company. A savings plan is a membership that provides discounts. Each has a specific purpose, and understanding the differences is the first step toward making an informed decision.

With in-house financing, you work directly with your trusted dental team. The application is typically simple, and approval often depends more on your relationship with the practice than a high credit score. Many of these plans offer 0% interest, which is ideal for paying off treatment over several months without extra costs.

In contrast, third-party lenders like CareCredit or Cherry function like a medical credit card or personal loan. The application is more formal and almost always requires a credit check. While they may offer longer repayment terms, you must be cautious of deferred interest. If the entire balance isn't paid by the end of the promotional period, you could be charged interest retroactively from the original date.

The Takeaway: In-house financing prioritizes simplicity and trust, making it excellent for short-term, interest-free payment plans. Third-party financing offers longer payment periods but involves a credit check and interest terms that require careful review.

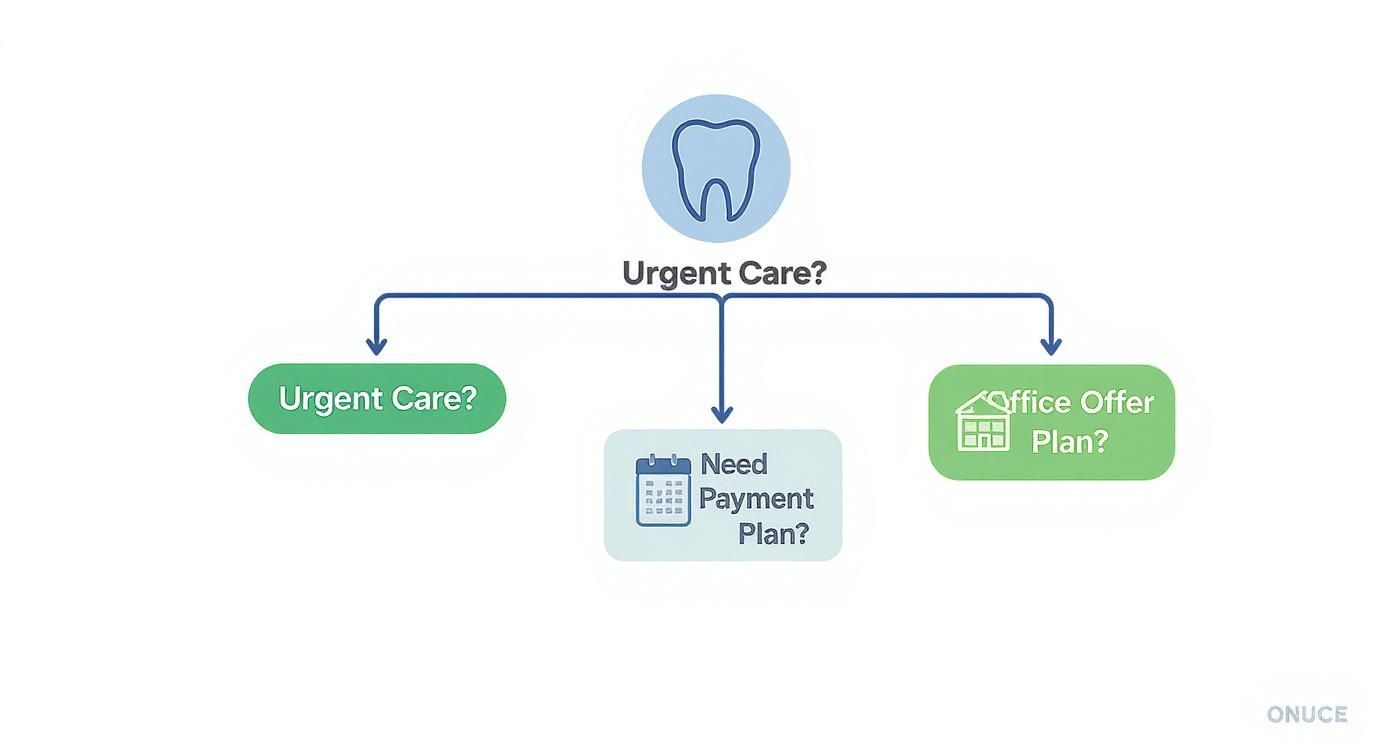

This decision tree can help you determine the best route for your specific situation by guiding you through key questions.

The flowchart guides you based on the urgency of your care, your need to split payments, and the options your dental office provides.

It is crucial to distinguish between financing and a dental savings plan. A savings plan, such as our Humble Savings Plan, is not a loan. It is a membership program where you pay an annual fee in exchange for significant discounts on nearly all services the office offers.

These two options can be used together effectively. For example, you could use a savings plan to reduce the total cost of your treatment. Then, you could use an in-house financing plan to pay off the smaller, discounted balance in manageable monthly installments. This combination is a powerful strategy for making dental care more affordable.

The global dental insurance market was valued at USD 201 billion in 2023, yet many people remain uninsured or underinsured, highlighting the importance of these alternatives.

Your credit history can also influence your choice. For a more detailed look, review our guide on financing dental work with bad credit. By comparing these approaches, you can find the financial path that best fits your budget and helps you achieve your treatment goals.

Dental in-house financing can be an excellent solution, but like any financial tool, it's important to consider it from all angles. Understanding both the benefits and potential drawbacks will help you determine if it's the right choice for you. For many, the advantages make it a clear winner.

The most significant benefit is often accessibility. Since you're making an arrangement directly with our practice, we can often be more flexible than a large financial institution. The focus is on your ability to manage payments, which opens the door to essential dental care for more of our patients.

Another major advantage is simplicity. You work with the same team you already know. There are no complex applications for external companies, no third-party websites to navigate, and no long waits for approval. Everything is handled in-office, and you can get clear, direct answers from a familiar face.

Let's focus on the most compelling feature: the potential for 0% interest. Many dental practices, including ours, offer plans with no interest charges. This means every dollar you pay goes directly toward your treatment, not to a lender. Over time, this can lead to substantial savings compared to using a high-interest credit card.

Here is a summary of the key benefits:

While in-house financing is a powerful tool, it's important to be aware of its limitations. One factor to consider is the shorter repayment term. Most in-house plans are designed for repayment within 6 to 18 months, which is shorter than a personal loan that might offer several years. This can result in higher monthly payments.

Remember, the financing plan is tied directly to the dental practice offering it. If you move or change dentists mid-treatment, the financing is not transferable. You would still be responsible for settling the balance with your original dentist.

Finally, consistent payments are crucial. Because this is a direct agreement, falling behind can strain your relationship with the practice. It could also result in late fees or a pause in your treatment. Before committing, ensure the monthly payment is a comfortable fit for your budget. By carefully weighing these points, you can make an informed decision that benefits both your smile and your finances.

The idea of applying for financing can seem daunting, but with dental in‑house financing, the process is designed for simplicity. Most dental offices are less concerned with a perfect credit history and more focused on your ability to make consistent payments. This patient-centric approach removes a significant barrier to receiving essential care.

Unlike a bank loan that scrutinizes your credit score, in-house plans are founded on the trust and relationship you have with your dental practice. The objective is to find a solution that works for you, not to judge your financial history.

To streamline the process, it’s helpful to gather a few documents beforehand. While each office has its own requirements, this list covers what is typically needed for an in-house financing application.

Actionable Tip: The goal is to create a partnership. Being prepared helps your dental team efficiently set up a plan that works for you without delays.

The most effective step you can take is to have an open conversation with the office manager. Be transparent about your budget and what you can realistically afford each month. This enables them to customize the dental in‑house financing terms to your specific situation.

It's also beneficial to ask if a down payment would be helpful. Offering a larger initial payment can sometimes reduce your monthly installments or lead to more favorable terms. The growth of the DSO market (Dental Service Organizations), which is projected to reach USD 294.34 billion by 2033, has helped standardize these patient-friendly options across the industry.

Ultimately, clear communication is key. It ensures you receive the treatment you need with a payment plan you can manage comfortably.

Considering how to pay for dental care often raises many questions. To provide clarity, we've compiled answers to some of the most common inquiries about dental in‑house financing. Our goal is to give you straightforward, factual information so you can make confident decisions.

Understanding these details will help you choose the best path forward for your oral health needs.

This is a major concern for many, and the short answer is typically no. Applying for a payment plan directly with a dental office usually does not impact your credit score. This is because most practices do not perform a "hard pull" on your credit report as a bank or credit card company would.

A dental office is more focused on your ability to meet the agreed-upon monthly payments rather than your entire credit history. It is always wise to confirm this with the office, but you can generally expect a simpler process without the worry of affecting your credit score.

Heads Up: While the application itself is unlikely to affect your credit, failing to make payments could. If an account becomes delinquent, the practice may report it to credit bureaus or send it to a collections agency, which would negatively impact your credit.

If you anticipate missing a payment, the most effective action is to contact your dental office immediately.

Because your agreement is directly with them, they are often more flexible and willing to work with you to find a solution. They may be able to adjust your due date or create a temporary arrangement to help you through a difficult period.

Ignoring the issue can lead to complications:

A proactive phone call can protect your finances and maintain a positive relationship with your dentist.

Yes, absolutely. In-house financing is an excellent option for cosmetic procedures, which are rarely covered by dental insurance. This includes popular treatments like veneers, professional teeth whitening, and adult orthodontics.

Since the financing is offered directly by the dental practice, it can be applied to any service they provide, whether it is medically necessary or for aesthetic purposes. This makes achieving your desired smile a realistic goal without requiring full payment upfront.

This is a common point of confusion, but they are two distinct financial tools that can be used together.

A dental savings plan functions like a membership club. You pay an annual fee to the dental office and receive significant discounts on most of their services. Its purpose is to lower the overall cost of your care.

In-house financing, conversely, is a payment plan. It is a method for dividing the cost of treatment into smaller, manageable monthly installments over a set period.

Here is the strategic advantage: You can combine them. Use your dental savings plan to secure a large discount on a major procedure, and then use the office's in-house financing to pay off the new, lower balance. This two-step approach makes even extensive dental work much more affordable.

At Clayton Dental Studio, we believe that financial concerns should not stand in the way of a healthy, brilliant smile. We offer a variety of flexible payment solutions, including our Humble Savings Plan and partnerships with trusted lenders, to ensure you receive the care you deserve. To learn more about our affordable options, visit us at https://www.claytondentalstudio.com.