Book Your Appointment Today!

Our staff will reach out to you shortly

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Yes, you can absolutely secure financing for dental work with bad credit. While it may seem daunting, several practical options exist, from direct payment plans offered by your dentist to specialized healthcare financing and personal loans designed for individuals with lower credit scores.

The key is to identify the most suitable path for your financial situation and the urgency of your dental needs. This guide provides actionable steps to navigate your choices.

Facing a dental problem while worrying about a low credit score creates significant stress. A throbbing toothache doesn't wait for your FICO score to improve, and the fear of being denied financing often causes people to postpone essential care.

This delay can escalate a minor, affordable issue into a major, costly procedure.

Consider this common scenario: you need an urgent root canal, but the $1,000+ cost feels insurmountable. The anxiety of a loan rejection is nearly as painful as the tooth itself. If this resonates with you, know that you are not alone.

Several factors contribute to the difficulty many Americans face in affording dental care. High treatment costs, significant gaps in dental insurance, and a shortage of affordable dentists have made financing a necessity for many.

Statistics highlight the scope of this issue. Approximately 57 million Americans reside in areas with a dental health professional shortage. Concurrently, treatment costs have risen steadily over the past two decades. With nearly one-third of Americans lacking any dental insurance, the entire financial responsibility falls on the patient.

It is no surprise that many must seek financing, even with a challenging credit history. You can explore these trends and their public health impact via the CDC.

The anxiety of needing dental work is significant, but the stress of figuring out payment can be debilitating. This guide aims to alleviate that anxiety by focusing on practical, actionable solutions to get you the care you need.

This guide provides a clear, step-by-step roadmap to secure the necessary financing. We will focus on the solutions that enable you to receive essential dental care without letting a credit score become an insurmountable barrier.

When you need a dental procedure and have a less-than-perfect credit history, the first step is knowing where to look for financial assistance. Let's review the most practical options, breaking down their suitability and what to expect. The goal is to find the right financial tool for your specific circumstances.

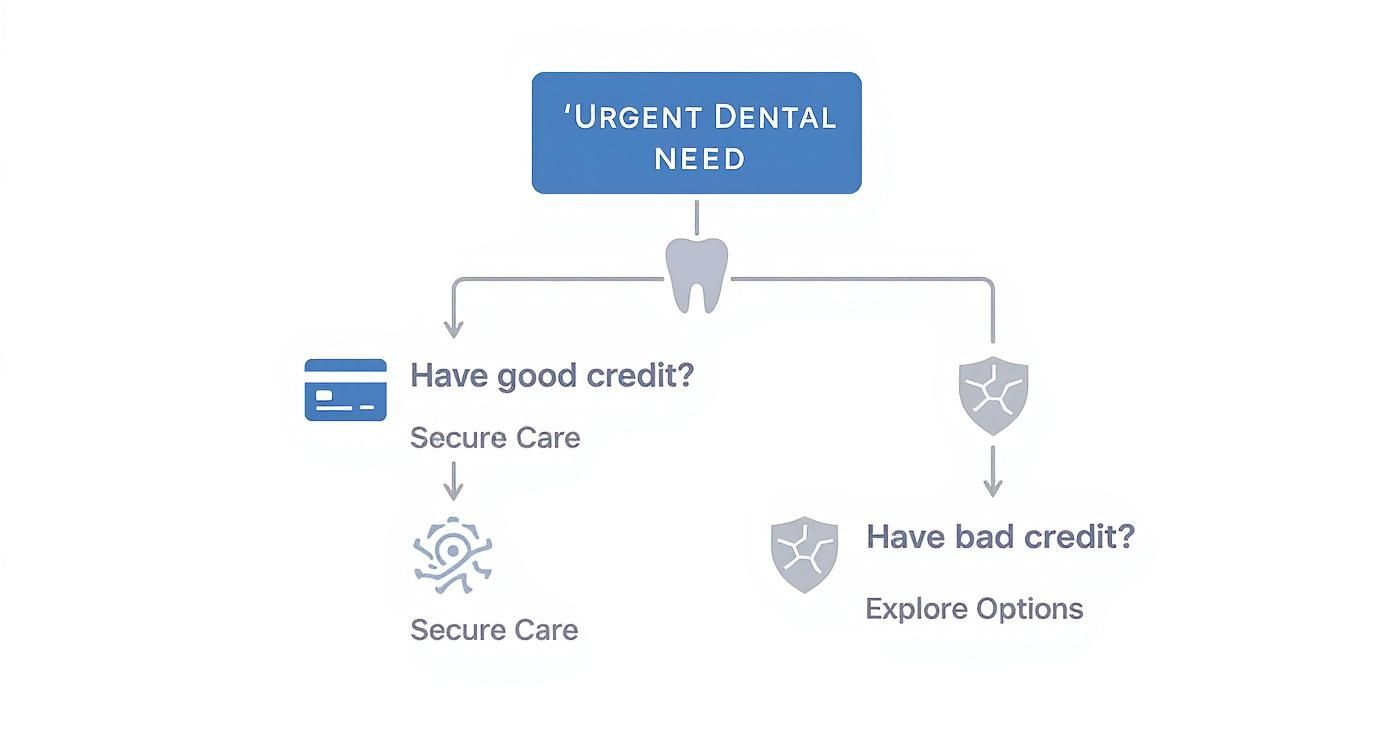

The decision tree below offers a visual guide to the initial thought process, illustrating different pathways based on credit status.

This flowchart illustrates a key point: while good credit provides straightforward options, bad credit simply requires exploring a different set of solutions. It is not a dead end.

Your first and often best option is right at your dentist's office. Many practices offer in-house payment plans, allowing you to pay for treatment in installments. Since the dental office makes the decision, approval often depends more on your relationship with them than on a formal credit check.

This is an ideal solution for small to medium-sized procedures, such as a crown or fillings, where the balance can be paid off within a few months. We explore how dental offices structure these options in our guide on how to afford dental work.

Companies like CareCredit and Cherry specialize in financing healthcare expenses, including dental work. They operate like credit cards but are exclusively for medical and dental costs. A significant advantage is that these lenders are often more flexible with credit scores than traditional banks.

For example, a provider like Cherry may approve applicants with scores as low as 520. The primary benefit is the ability to cover larger expenses—such as dental implants or orthodontics—and spread payments over a longer term. Look for their promotional 0% APR periods, which can significantly reduce costs.

To clarify your choices, this table compares common financing methods, focusing on the factors that matter most when dealing with a low credit score.

The right choice depends on your specific needs and the total cost of your treatment. Don't hesitate to ask your dental office for their direct recommendations.

A personal loan is another viable option, particularly for consolidating the cost of extensive procedures into a single, predictable monthly payment. While some traditional banks have strict criteria, many online lenders now consider factors beyond your credit score, such as income and employment stability.

Medical debt can negatively impact a credit score. A 2024 KFF survey found that 40% of U.S. adults have some form of healthcare debt. When financing dental work with bad credit, expect higher interest rates, typically from 15% to 36% APR. However, some platforms now offer no-credit-check loans up to $25,000, providing a crucial resource.

An in-house plan may be suitable for a $1,500 crown, while a $5,000 bridge might be better financed through a third-party lender. Understanding these options is the first step toward choosing the right financial tool for your treatment plan and budget.

A financing denial can be disheartening, especially with a pressing dental issue. However, a denial is not the end of the road. It is a signal to explore alternative strategies to get the care you need.

When standard lenders are not an option, the most effective next step is to strengthen your application. A co-signer can make a significant difference.

Asking a trusted family member or close friend with a strong credit history to co-sign your application can be the most effective way to turn a denial into an approval. A co-signer provides the lender with a guarantee that payments will be made, reducing their risk.

This often results in approval and may also secure a lower interest rate. However, this is a significant request with serious responsibilities for both parties.

Before approaching someone, be prepared for a transparent conversation.

A co-signer is a financial partner in your dental health. Treat this relationship with transparency and respect to preserve your personal bond long after the debt is repaid.

Effective solutions can often be found within your local community. Many areas have resources designed to provide affordable dental care, independent of credit scores and lenders. These programs prioritize need over financial history.

A bit of research can lead to significant savings.

These community-focused options are ideal alternatives for financing dental work with bad credit because their mission is public health, not profit. Exploring these programs can help you find quality care that fits your budget, proving that a financing denial does not have to prevent you from achieving a healthy smile.

When seeking to finance dental work with a low credit score, proactivity is your greatest asset. Instead of passively submitting applications, take strategic steps to improve your chances of approval and secure better terms. This is about transitioning from a passive applicant to an empowered patient.

An effective first step is to review your credit report before applying. You can get free copies from all three major bureaus—Equifax, Experian, and TransUnion—at AnnualCreditReport.com. Identifying and disputing errors, such as a paid-off account still showing a balance, can provide a quick boost to your score.

The credit reporting landscape is evolving, particularly regarding medical debt. In 2023, major credit bureaus stopped including paid medical collections and any medical debt under $500 on consumer reports. This change reflects a growing recognition that unexpected medical bills are not indicative of overall financial risk.

This is a significant advantage if old dental bills are weighing down your credit score; they may not be as detrimental as you assume. This knowledge empowers you during discussions with lenders and your dental office. You can learn more about how federal rules on medical debt are changing to protect consumers.

Your dentist’s office manager or financial coordinator can be your strongest ally. Their role is to help you find a viable path to treatment. Do not hesitate to have a direct and honest conversation with them about your situation.

Offering a larger down payment is a powerful negotiation tool. If you can pay 20-30% of the total cost upfront, you significantly reduce the practice's financial risk. This single action often makes them more agreeable to setting up a flexible in-house payment plan for the remaining balance.

Here is a script you can adapt for that conversation:

"I have my treatment plan and am ready to proceed. I can make a down payment of [Your Amount] today. Would it be possible to arrange a direct payment plan for the remainder over the next six months?"

This approach demonstrates that you are serious and responsible, making them more inclined to work with you. For larger procedures, it helps to understand the associated costs. Our guide on how much dental implants cost provides valuable context. Being informed allows you to discuss financing with confidence and advocate for a plan that aligns with your budget.

Navigating dental financing with imperfect credit can feel overwhelming, but a structured, step-by-step plan makes the process manageable. This roadmap will guide you from understanding your needs to securing the funds for your treatment.

Follow these steps to move closer to a healthy smile.

Before applying for financing, preparation is crucial. A clear understanding of your treatment needs and budget forms the foundation for all subsequent steps.

This preparation is about taking control. When you are armed with complete information, you can make financial decisions from a position of confidence, not desperation.

With your preparations complete, it is time to actively seek financing. The key is to explore multiple options to find the best fit for your situation rather than accepting the first offer.

Navigating dental financing with a low credit score naturally raises many questions. Getting clear answers can provide the confidence needed to move forward with treatment.

Here are some of the most common concerns we address.

Yes, many no credit check financing options are legitimate, but it is crucial to proceed with caution. These lenders manage risk differently, which typically translates to higher costs for the borrower.

Instead of a FICO score, they may evaluate other factors like income stability or bank account history. Due to the increased risk they assume, these loans almost always have higher interest rates and fees. A reputable company will be transparent about these costs.

Watch for these red flags:

This is an excellent question. The credit scoring system distinguishes between "soft" and "hard" inquiries.

Most lenders now use a soft inquiry for pre-qualification. This gives them a preliminary look at your credit profile to estimate potential rates and has zero impact on your score. You can pre-qualify with multiple lenders without any negative effect.

A hard inquiry occurs only when you formally apply for a loan. This can cause a temporary dip of a few points in your score. However, credit bureaus recognize that consumers shop for the best rates. If you submit all your formal applications within a short period—typically 14 to 45 days—they are treated as a single credit event.

The actionable takeaway: Pre-qualify with as many lenders as you wish, as it is free and does not harm your score. Once you identify the best offer, submit your formal applications within a consolidated timeframe to minimize the impact on your credit.

Unexpected life events can disrupt your financial stability. If you are approved for a loan but later find you cannot manage the payments, the most important step is to be proactive. Do not wait until you miss a payment.

Contact the lender or financing company immediately. Explain your situation honestly and ask about your options. Most companies prefer to work with you to find a solution rather than initiate collections.

Potential solutions they may offer include:

Ignoring the problem is the worst course of action, as it leads to late fees, credit damage, and collections. A simple, honest phone call is your most effective tool for getting back on track.

At Clayton Dental Studio, we believe that clear information and accessible options are essential for enabling quality dental care for everyone. If you have questions about our in-house savings plan or our partnerships with CareCredit and Cherry, our team is here to guide you. Let's find a practical solution to get you the care you deserve. Explore your options with us at https://www.claytondentalstudio.com.