Book Your Appointment Today!

Our staff will reach out to you shortly

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Staring down a significant dental bill can be daunting. You're not alone in feeling this way. Quality dental care is a crucial investment in your health, but the costs for procedures like crowns, root canals, or cosmetic work can add up quickly. The first step toward managing these costs is to understand them.

Why does essential dental work come with a high price tag? It's a combination of factors: the cost of durable, high-quality materials, the sophisticated technology used in a modern dental office, and the years of specialized training required to perform complex procedures safely and effectively.

For example, a single, high-quality porcelain crown can range from $800 to $3,000, depending on the material and location. If you're considering a full smile makeover, understanding how much veneers cost can also be an eye-opening part of the planning process.

This financial reality is amplified when you consider how many people lack adequate dental insurance. While the global dental service market is projected to reach USD 680.30 billion by 2032, millions of individuals must navigate these costs on their own.

By the end of 2023, nearly 68.5 million adults in the U.S. had no dental coverage. This situation often forces people to delay or skip essential treatments, which can lead to more complex and expensive health problems in the future.

The good news is that affordable, top-tier dental care is attainable. It's not about finding a single solution, but about understanding all your options and creating a financial plan that works for you.

This guide provides practical, actionable strategies to help you manage costs without compromising your oral health.

We will cover:

Insurance & Membership Plans: How to maximize your benefits or find effective alternatives.

Financing & Payment Options: Strategies to break down large costs into manageable payments.

Community & Non-Profit Resources: How to access assistance from grants and low-cost clinics.

The Power of Prevention: How proactive habits can save you thousands of dollars over time.

By combining these approaches, you can build a clear, manageable plan to move forward with the dental care you need.

Your dental insurance plan is your first line of defense against high dental costs, but policies can be confusing. Misinterpreting the terms can lead to unexpected bills, which is a stressful and avoidable situation.

Let's break down the jargon so you can use your benefits with confidence.

Think of your insurance policy as a cost-sharing agreement. You pay a monthly premium, and in return, your insurance company covers a portion of your dental care expenses. However, this coverage has specific limits and rules defined by a few key terms.

Understanding three main components of your plan will help you predict your out-of-pocket costs and avoid financial surprises.

Deductible: This is the fixed amount you must pay for covered services before your insurance company begins to pay. For example, if your deductible is $50, you are responsible for the first $50 of treatment costs.

Copayment (or Coinsurance): After your deductible is met, you share the cost with your insurer. This can be a flat fee (copay) or a percentage (coinsurance). If your plan covers crowns at 80%, you are responsible for the remaining 20%.

Annual Maximum: This is the total amount your insurance plan will pay for your dental care within a plan year. If your annual maximum is $1,500, any costs beyond that amount are 100% your responsibility until the plan resets.

Actionable Tip: Before committing to a major procedure, ask your dentist's office to submit a pre-treatment estimate to your insurance provider. This document requires the insurance company to state in writing what they will cover and what your estimated share of the cost will be, eliminating guesswork.

What if you don't have insurance? Many modern dental practices, including Clayton Dental Studio, offer an in-house membership plan as a direct and simple alternative.

Instead of paying premiums to an insurance company, you pay a flat annual fee directly to the dental office.

This fee typically covers all your preventive care for the year—such as cleanings, exams, and routine X-rays—and provides a significant discount on other restorative or cosmetic procedures.

Our Humble Savings Plan, for instance, was designed to make exceptional dental care predictable and affordable. With a plan like this, there are no deductibles, waiting periods, or annual maximums. You receive the care you need at a clear, discounted price, making it a straightforward way to budget for your family's dental health without the complexities of traditional insurance.

Even with a solid insurance or membership plan, some treatments involve a significant upfront cost. When you need care immediately but cannot cover the full amount at once, financing options can bridge the gap. Understanding how they work is key to using them effectively.

Third-party financing, often in the form of a healthcare credit card, is a common tool for breaking down a large bill into smaller, predictable monthly payments. This approach helps many people access necessary care without depleting their savings.

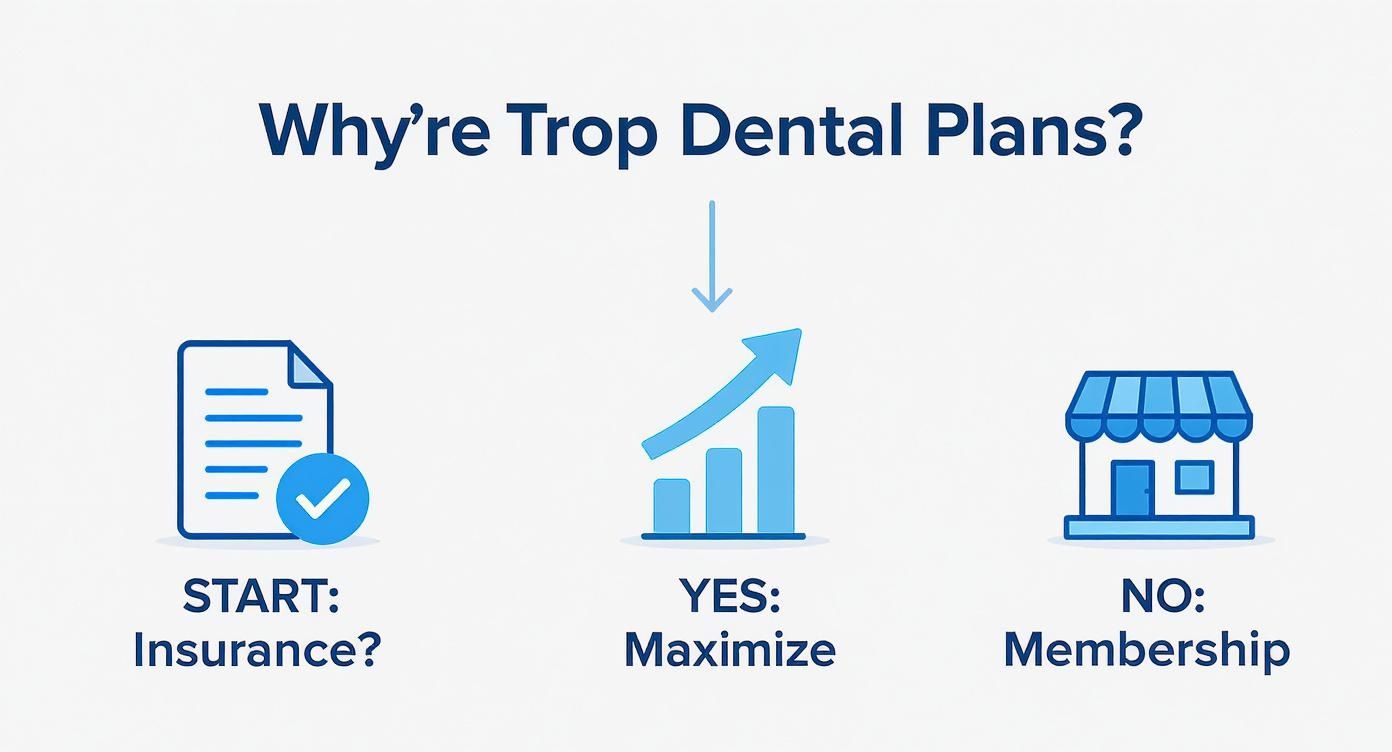

This decision tree illustrates a practical approach to planning your dental expenses.

As shown, the first step is always to evaluate your existing coverage before exploring alternatives like membership plans or other payment strategies.

Companies like CareCredit and Cherry offer credit cards specifically for health, wellness, and dental expenses. Their main appeal is the promotional periods that offer 0% interest for a set time—often 6, 12, or 24 months.

This can be an excellent option, provided you can pay off the entire balance before the promotional period ends. Be aware that if any balance remains after the deadline, high interest rates are often applied retroactively to the original purchase amount. Always read the terms carefully and have a clear plan to pay off the balance in time.

Treat these 0% offers as short-term, interest-free loans. Calculate your required monthly payment by dividing the total cost by the number of months in the promotional period. Paying at least this amount each month will ensure you avoid unexpected interest charges.

Seeing your options side-by-side can help clarify the best path for your situation. Here is a breakdown of the most common ways to finance dental work.

Each method provides different benefits. The right choice depends on your specific treatment plan, credit history, and comfort level with various payment structures.

Don't overlook the simplest solution: discussing an in-house payment plan directly with your dentist's office. Many practices, including Clayton Dental Studio, are willing to work with patients to create a payment schedule that fits their budget.

These plans offer significant advantages:

No Interest: Most in-house plans are interest-free.

No Credit Check: Your relationship with the office is what matters, not your credit score.

Flexibility: Plans can often be customized based on your financial situation and treatment timeline.

For example, if you need a procedure that requires multiple visits over several months, an in-house plan allows you to pay for the work as it is completed. This makes complex treatments like dental implants feel much more manageable. You can get a better sense of the investment by reading our guide that explains how much dental implants cost and the factors that contribute to the final price.

The best first step is always a direct conversation with your dental office's financial coordinator. They can explain every option available, from third-party lenders to flexible in-house arrangements, helping you find a solution that provides the care you need without financial strain.

While finding the right payment solution is important, the most effective way to afford dental work is to minimize the need for extensive treatment. This requires a shift from a reactive to a proactive mindset.

Making small, consistent investments in your oral health now can help you avoid major, costly interventions later.

One of the most effective tools for managing healthcare costs is a tax-advantaged savings account. If your employer offers a Health Savings Account (HSA) or Flexible Spending Account (FSA), it can be a game-changer for your dental budget.

These accounts allow you to set aside pre-tax money for medical and dental expenses. This means you pay for cleanings, fillings, crowns, and orthodontics with untaxed dollars, giving you an automatic discount on every procedure.

Here’s a quick overview:

HSAs are typically linked with high-deductible health plans. The funds roll over each year and can be invested, making it an excellent long-term healthcare savings tool.

FSAs are more common but usually have a "use it or lose it" rule, requiring you to spend the funds within the plan year.

If you are in the 22% tax bracket, paying for a $1,000 dental procedure with an HSA or FSA is equivalent to an instant $220 discount. These savings add up significantly over time.

The financial case for preventive care is clear. A routine cleaning and exam may cost around $100, but this is the appointment where a small cavity can be detected before it becomes a major problem.

An untreated cavity can grow, leading to the need for a root canal and crown—a procedure that can easily cost $2,000 or more.

That $100 preventive visit is your best investment. It represents the difference between a minor, affordable fix and a complex treatment that costs 20 times as much. Committing to regular check-ups is the single most effective way to protect your smile and your finances.

This is why understanding how often you should visit the dentist is not just a health question—it's a critical financial one.

Never hesitate to talk openly with your dental team about your budget. We are your partners in health, and that includes your financial well-being. A good dental team will respect your concerns and work with you to create a treatment plan that aligns with your financial reality.

For instance, if you require several procedures, we can help prioritize them. We will address the most urgent issues first and phase the remaining treatments over several months or into the next insurance plan year to help you maximize your benefits.

This collaborative approach ensures you receive essential care promptly while creating a manageable, long-term plan. Your oral health journey is a partnership built on clear and honest communication.

Navigating the financial side of dental care often raises specific questions. Let’s address some of the most common concerns we hear from patients trying to make their dental work more affordable.

This is a common and understandable concern. The best course of action is to communicate openly with your dental team. A professional team will work with you to find a solution, which often involves phasing your treatment.

This means we review your entire treatment plan and prioritize what is most urgent—addressing pain, infection, or problems that will worsen and become more expensive over time. We tackle those issues first, then schedule less critical procedures over the following months. This approach allows you to spread out the cost and fit it into your budget without compromising your long-term health.

Using a standard credit card should be a last resort. The high-interest rates on most consumer credit cards can significantly increase the total cost of your treatment. A $2,000 procedure on a card with a 20% interest rate could accumulate hundreds of dollars in interest by the time it's paid off.

Before using a regular credit card, explore dedicated healthcare financing options like CareCredit or Cherry. They often offer promotional periods with 0% interest, which are designed for this purpose and can save you a substantial amount of money if you pay off the balance before the term ends.

An estimated 41% of U.S. adults carry debt from medical or dental bills. Choosing the right financing tool is a critical step in ensuring your dental care does not become a long-term financial burden.

While you generally cannot negotiate the fee for a specific procedure like a crown, you can—and should—discuss the overall financial plan. Many dental practices offer options that can reduce your total out-of-pocket cost.

It is always worth asking about:

Pay-in-Full Discount: Some offices offer a small discount (often around 5%) if you can pay for the entire treatment upfront with cash or a check. This helps them avoid credit card processing fees, and they can pass the savings to you.

New Patient Specials: If you are new to a practice, check its website for introductory offers for exams, cleanings, and X-rays.

Membership Plan Perks: If you belong to an in-house savings plan, ask about additional discounts on major procedures. Members often receive a better rate than the standard fee.

The goal is to work collaboratively to find all available tools to make your care affordable. An open conversation about your budget is the best way to start.

At Clayton Dental Studio, our mission is simple: we want everyone to have a healthy, confident smile without financial anxiety. Dr. Kamboj and our entire team are committed to providing clear, transparent pricing and flexible solutions that work for your family. Whether it's phasing your treatment, setting you up with our Humble Savings Plan, or finding the right financing option, we are here to support you.

Schedule your appointment today and let us partner with you on your journey to excellent oral health.