Book Your Appointment Today!

Our staff will reach out to you shortly

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Think of a dental membership plan much like your gym subscription: you pay a predictable fee and in return you get routine cleanings and exams. Beyond that, there’s an entire roster of dental insurance alternatives—from in-house membership plans to discount networks, HSAs/FSAs, financing options like CareCredit and Cherry, dental school clinics, community clinics, self-pay negotiations, and even setting up a dedicated emergency fund. Each pathway changes how you budget, schedule visits, and handle the paperwork. Use this guide to narrow your choices, take action, and lock in savings.

Your aim is simple: align oral health habits with a model that fits your wallet.

Action Steps:

Membership plans reward consistent care while discount networks suit occasional visits.

In-House Membership Plan

Benefit: predictable flat fee for exams and cleanings

Drawback: care limited to that practice

Action: Request plan details and service caps

Discount Network

Benefit: pre-negotiated service fees at multiple practices

Drawback: membership dues and varying discount levels

Action: Compare two networks’ fee schedules

HSA/FSA

Benefit: healthcare dollars grow tax-free

Drawback: “use-it-or-lose-it” rules each plan year

Action: Calculate max contributions now

CareCredit or Cherry Financing

Benefit: split big bills into smaller payments

Drawback: interest applies if not paid off in promotional period

Action: Pre-qualify online to check rates

Dental School Clinics

Benefit: 30–70% lower fees under faculty supervision

Drawback: longer appointments and student practitioners

Action: Book your slot 6–8 weeks ahead

Community/Charity Clinics

Benefit: sliding-scale pricing based on income

Drawback: limited hours and appointment availability

Action: Gather income documents in advance

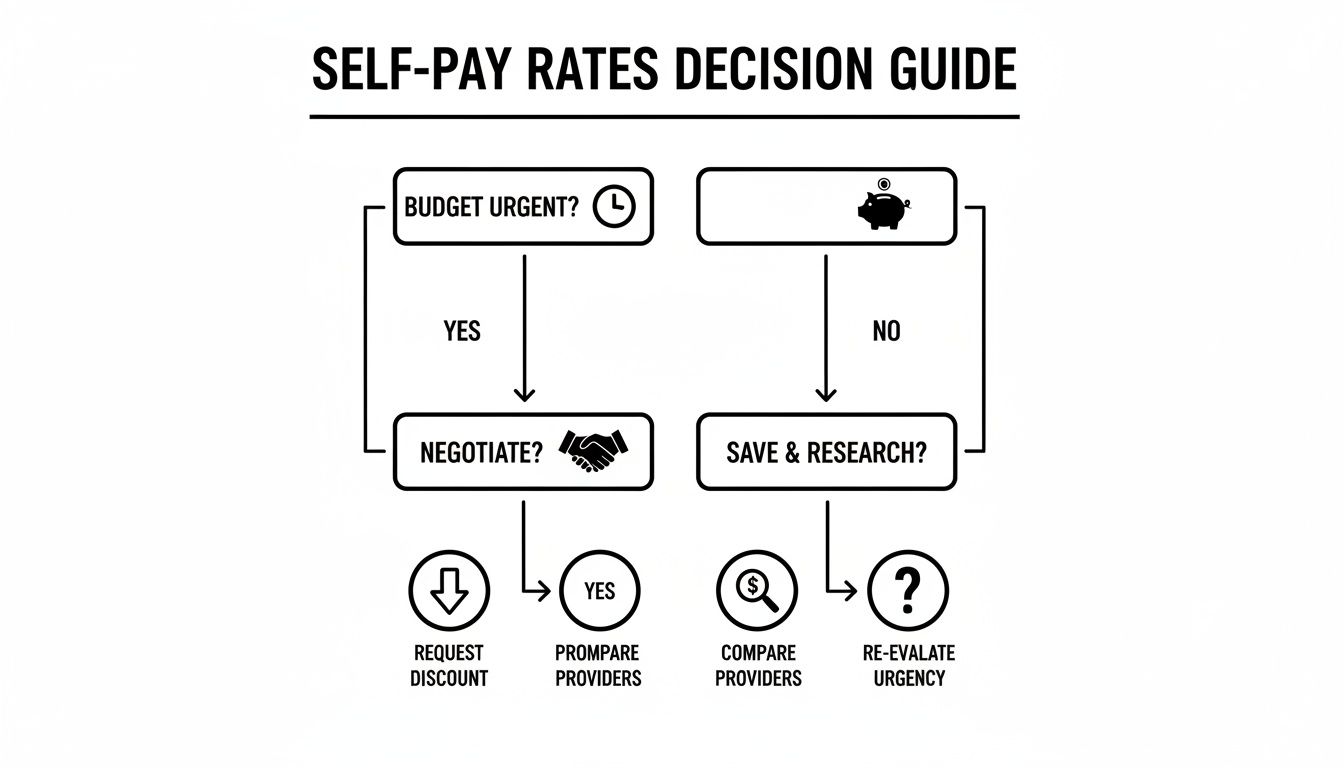

Negotiated Self-Pay

Benefit: haggle directly for 5–20% off

Drawback: requires research and confident negotiation

Action: Collect 3 local price quotes

Dental Emergency Fund

Benefit: no interest, no fees—just your own savings

Drawback: discipline needed to sock money away

Action: Automate monthly deposits

Use your answers to these factors to narrow to your top two options.

For a deeper dive into local options, see our post on Affordable Dental Care in Houston.

Membership plans work like subscription services: you pay a flat fee, then receive fixed discounts on routine and common procedures. Discount networks, by contrast, negotiate rates across practices so you pay a reduced fee each time.

Sara, a freelance graphic designer, slashed her twice-yearly cleanings by 50% with an app-based membership. Action: Compare an in-house plan with a discount network by requesting both providers’ fee schedules.

Dentist bills you directly with an annual or monthly fee. You unlock discounts instead of dealing with insurance claims.

Key Aspects To Evaluate:

Example Plans:

Action Step: Ask for sample member bills to see real savings.

You pay an annual fee, then use a card or code at various offices to access reduced rates.

Watch For:

Action Step: List top three networks and check provider directories.

“Membership plans guarantee direct savings at the source while discount networks rely on bargaining power across practices.”

Action: Rank fee vs. savings on your decision matrix.

Before committing, ask:

Tally your expected visits and costs, then match with plan features. Over the last decade, consumers have shifted toward these lower-cost alternatives. See trend details at Mordor Intelligence.

Stash pre-tax money into an HSA or FSA to lower taxable income and have funds ready for care. Use these accounts to make routine work nearly 30% cheaper.

Action Steps:

When HSA/FSA falls short, split costs with financing.

Action: Pre-apply to see your personalized rates.

A dental loan is most sensible when you need to cover unexpected major procedures without dipping into savings.

Learn more about dental insurance market projections. For no-insurance financing advice, see dentist payment plans without insurance.

Action: Match procedure size to financing term.

Dental schools offer 30–70% savings under expert supervision. Community clinics use sliding scales for low costs.

Maria paid $85 for cleaning and X-rays that usually cost $200.

Action: Compare wait times vs. savings.

Action: Prepare documents and set calendar alerts.

Charity days often serve patients up to 200% of the federal poverty level.

Once you’ve pinpointed clinics, bookmark portals and register immediately when slots open. Clayton Dental Studio’s Humble Savings Plan also offers instant relief—no long waits.

Start with an itemized fee schedule and negotiate confidently. Treat it like shopping with full price tags.

“Bringing competitor quotes can easily shave off an extra 10 percent or more,” says a local Humble dentist.

Open a “Dental Care Fund.” Automate $50 monthly transfers.

Best Practices:

Action: Set up automatic transfers today.

Track every expense with:

“Consistent tracking and small adjustments prevent budget shortfalls,” advises a financial planner.

Define your annual dental budget by listing expected services and local costs. Then map options against convenience and cost.

Next to each, jot down cost estimates. Compare totals to:

Plot convenience (Y-axis) vs. cost (X-axis).

Action: Create your own matrix and score each option.

Each step takes under ten minutes—fit into a coffee break.

With a clear budget, decision matrix, and these step-by-step actions, you’ll enroll quickly and start saving on routine and unexpected treatments. Acting today can save you hundreds by next year.

Taking action today on your dental insurance alternative can save you hundreds of dollars by next year.

What Are the Main Cost Differences Between Discount Plans and Traditional Insurance?

Discount plans slash 15–50% off rates with set fee schedules. Traditional insurance uses deductibles and annual maximums (often $1,500 cap).

Can I Use HSA Funds for Cosmetic Procedures?

IRS rules allow HSA withdrawals only for treatments that address dental disease or prevent health issues. Cosmetic services (whitening, veneers) need documented medical necessity.

Can I Use HSA Funds for Necessary Veneers?

Requirements:

“HSAs cover restorations but not elective cosmetic care,” the IRS guidelines emphasize.

How Do I Find a Reputable Community Clinic?

What Should I Ask in a Self-Pay Negotiation?

With these actionable insights and informative steps, you’ll walk into your next appointment fully prepared and confident.

For tailored savings plans and new-patient specials visit Clayton Dental Studio.