Book Your Appointment Today!

Our staff will reach out to you shortly

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

If you're in Humble or the Houston area and you've ever looked at a dental estimate, closed the tab, and told yourself you'll deal with it later, you're not alone. A lot of families are in that exact spot. The kids need checkups, someone has a cracked tooth, or you've been putting off a crown because the timing never feels right.

Dental costs hit families in a very real way. They compete with groceries, rent, school expenses, and car repairs. When money is tight, even people who care about their health can end up delaying treatment because they need a plan they can realistically afford.

A common scene in many households looks like this: one parent is checking the family budget, another is trying to compare insurance options, and a child is overdue for a cleaning. Nobody is ignoring their health on purpose. They're trying to make the numbers work.

That pressure is widespread. According to a survey by the Oral Health Institute, 59% of respondents cited cost as the top reason for avoiding the dentist, and 46% of Americans skip or postpone dental treatments due to expense (Penn Dental Medicine on affordable dental care).

For many families, the hardest part isn't the procedure itself. It's the uncertainty. You may not know whether insurance will help, whether the office offers payment options, or whether a lower-cost clinic is realistic for your schedule.

That uncertainty often leads to delay. Delay turns small problems into bigger ones. A tooth that needed a simple fix can become a larger restorative issue if it keeps getting pushed back.

Practical rule: If cost is the reason you're hesitating, ask about payment structure before you decide against treatment. The right financial path often matters as much as the treatment plan itself.

People often assume affordable care means sacrificing quality, or that if they need help paying, they're out of options. That's not how modern dental care works. There are several legitimate affordable dental care options, and they don't all fit into the same category.

Some families do better with insurance. Others prefer an in-house savings plan because it removes paperwork and annual limits. Some need financing for a larger treatment, while others benefit most from a community clinic or a dental school.

What matters is matching the option to your situation. If you're a middle-income family in Humble who doesn't qualify for low-income programs but still can't justify expensive premiums, there are workable paths forward. You don't need guesswork. You need clarity.

Individuals often feel overwhelmed by grouping all cost-saving strategies together. This makes it difficult to evaluate what fits your household. In practice, there are four main pathways, and each solves a different problem.

A range of solutions exists to make dental care more accessible, including government-supported Federally Qualified Health Centers with sliding scales, low-cost care at dental schools, Marketplace plans with pediatric dental coverage, and direct-to-practice membership plans (MouthHealthy guide to finding affordable dental care).

Think of these options the way you might think about paying for a car. Some people want the predictability of a monthly structure. Others need a short-term financing solution. Some qualify for public resources. Dentistry works the same way.

The wrong approach is choosing based on label alone. "Insurance" sounds safe, but that doesn't always mean it's the best fit. "Low-cost clinic" sounds affordable, but the trade-offs may not work for your schedule, especially if you're juggling school pickups, work shifts, and transportation.

For orthodontic questions, families also benefit from comparing options carefully instead of assuming one path is automatically cheaper. If you're researching alignment outside the U.S. or just want a plain-English comparison model, this guide to affordable teeth straightening methods in the UK is useful because it shows how treatment choices, supervision level, and payment structure all affect real-world affordability.

A good first step is learning how alternatives to traditional insurance are structured in a private practice setting. This overview of dental insurance alternatives is helpful if you're trying to compare a direct membership model with standard coverage.

Affordable care isn't one product. It's a payment strategy that matches your family's needs, timing, and tolerance for paperwork.

This is the comparison many Humble families care about most. They aren't necessarily looking for free care. They want something manageable, understandable, and worth paying for.

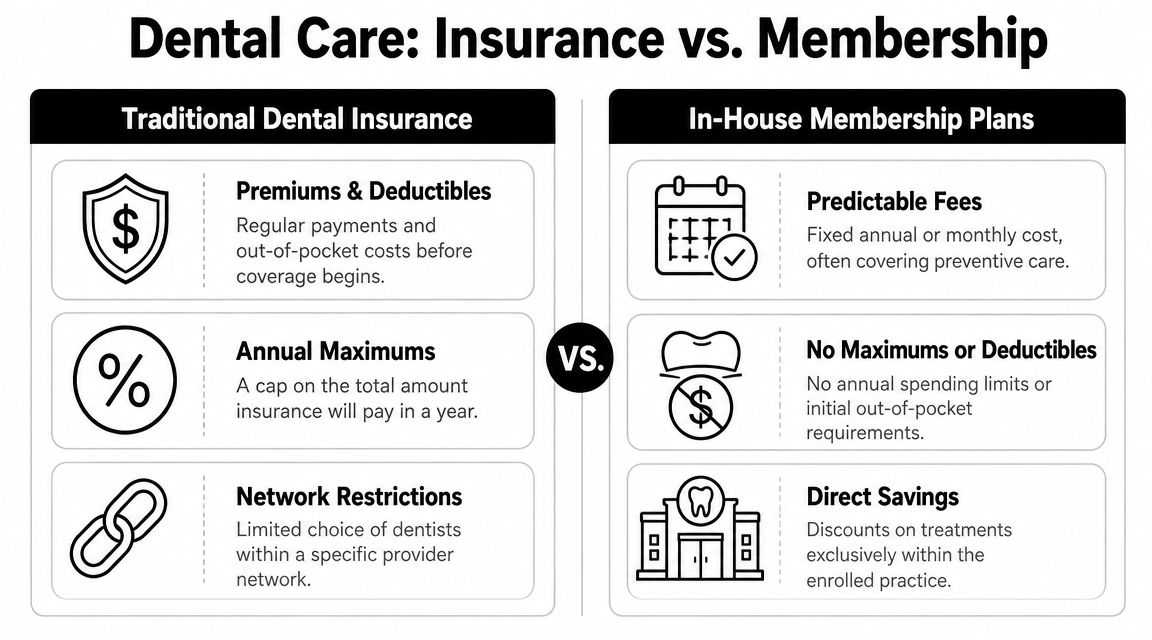

Traditional dental insurance can help, but it comes with rules. Dental insurance typically covers preventive services at 100%, basic procedures at 70 to 80%, and major work at 50%, with annual maximums often capping around $1,000 to $1,200. In-house membership plans offer a parallel structure, with monthly costs comparable to insurance premiums but without the claim processing, waiting periods, or annual caps (Delta Dental of Washington on dental benefits affordability).

Insurance works best for patients who:

But insurance also creates friction. Annual maximums can run out quickly once you need a crown, root canal, bridge, or implant-related treatment. Networks can also limit where you go, and pre-authorization or claims processing can slow down decision-making.

An in-house membership plan is simpler. You pay the practice directly, usually through a fixed annual or monthly amount, and you receive included preventive services plus reduced fees on additional treatment. There are no insurance claims because it isn't insurance.

For middle-income families, that simplicity matters more than people expect.

Here's where these plans often make sense:

| Situation | Insurance | In-house membership |

|---|---|---|

| Routine cleanings and exams | Often covered well | Often included directly |

| Paperwork and claims | Required | Minimal |

| Annual spending cap | Common | Not built around annual maximums |

| Network restrictions | Possible | Tied to one office by design |

| Predictability | Moderate | High for preventive care |

A membership plan is usually strongest when you want an ongoing relationship with one office and straightforward pricing. It isn't the same as broad insurance portability. If you move frequently or prefer to shop among many network offices, traditional insurance may feel more flexible.

If your family is trying to compare broader medical and dental coverage together, this breakdown of comprehensive family health plans in Florida is a useful example of how bundled benefits are structured, even though plan rules vary by state.

One private-practice example in Humble is Clayton Dental Studio, which offers the Humble Savings Plan as a direct membership option with tiered benefits for kids and adults, plus discounts on additional treatment. That kind of model can work well for families who want preventive care covered in a predictable way and would rather avoid insurance administration.

The best choice is usually the one you'll actually keep using. A plan that looks good on paper but feels confusing every time you need care often doesn't save money in real life.

The biggest financial shock in dentistry usually isn't a cleaning. It's the treatment you didn't expect. A crown after a cracked tooth. A root canal after pain wakes you up at night. An implant consultation after a tooth can't be saved.

That's where financing matters. Public resources don't always address this well, especially for working families who are above assistance thresholds but still can't absorb a large bill all at once. A significant gap in public resources is the lack of information on financing for working families who don't qualify for low-income aid but can't afford high insurance premiums. Third-party financing and in-house payment plans bridge this divide, addressing a critical need for the nearly 33% of Americans without dental coverage (San Fernando Valley Dental Society low-cost dental care resource).

Financing turns a large treatment fee into smaller scheduled payments. In dentistry, families often see this through companies such as CareCredit or Cherry. The office submits the amount for approved treatment, and the patient repays according to the terms of that financing arrangement.

That changes the conversation from "Can we afford this total?" to "Can we afford this monthly payment?" For many households, that's the difference between moving forward and delaying care.

Not all financing is equal. Before choosing a plan, ask:

A more detailed look at dentist payment plans with no insurance can help you prepare for that conversation before you schedule treatment.

Here is a short overview that helps explain why many patients prefer monthly structures for larger care decisions:

Financing is not a discount. It doesn't replace preventive care, and it doesn't make every treatment inexpensive. What it does is improve timing and predictability. If the dental need is immediate, spreading cost over time can be the most practical option.

It also works best when the treatment plan is clear. Patients should understand what is urgent, what can be phased, and what can wait. Good offices will discuss those distinctions openly so you aren't financing work blindly.

Community clinics and dental schools are legitimate options, and for some families they are the right answer. They exist to expand access, not to provide luxury convenience. When cost is the top issue, they deserve serious consideration.

Federally Qualified Health Centers and dental school clinics can reduce treatment costs by 40 to 70% using income-based sliding scales or by charging only for materials. However, geographic disparities can mean travel times of 45 to 60 minutes for patients in rural or underserved areas, compared to a 15-minute urban benchmark (NIDCR guide to finding low-cost dental care).

These options often work well for patients who:

Dental schools can be especially valuable for preventive and restorative treatment when patients don't mind longer appointments. Supervising dentists oversee the care, which gives many patients confidence in the process.

Reduced fees don't automatically mean easy access. Availability can be limited, waitlists can be longer, and appointment times may not fit a busy family schedule. If you work hourly shifts, coordinate childcare, or need same-day attention, those limits matter.

Community-based care is also less ideal when speed is essential. A family trying to manage ongoing work, school, and transportation may decide that a local private office with a savings plan and financing is worth the difference in cost because it reduces missed work and missed school.

Lower fees help, but convenience has value too. A delayed appointment can become expensive in its own way if pain worsens or treatment gets larger.

The right answer depends less on the label and more on your situation. Families in Humble usually aren't choosing between "good" and "bad" options. They're choosing between different trade-offs: lower fees versus faster scheduling, broad coverage versus simpler pricing, or immediate treatment versus staged treatment.

An in-house membership plan is often the cleanest fit for families who don't want to deal with insurance claims and just want routine care handled in a straightforward way. This is especially practical for freelancers, self-employed parents, and households paying out of pocket.

If you're weighing local options, this guide to finding an affordable dentist in Humble, TX gives a useful starting point for comparing what nearby offices offer.

Financing is often the better tool. This is common with crowns, implants, larger restorative cases, or urgent pain. If the problem is time-sensitive, the ability to split treatment cost into monthly payments may matter more than whether the office accepts a particular insurance plan.

Community clinics and dental schools deserve a close look. They may require patience and flexibility, but they can reduce fees in a meaningful way. If transportation and scheduling are workable, they can be a practical path to care.

For families with children, simplicity matters. You want to know what's included, what happens if a child needs X-rays, and how emergency visits are handled. The more complicated the payment system, the more likely people are to postpone routine care.

A useful way to decide is to ask these four questions:

For many Houston-area middle-income families, the most practical combination is routine care through a membership plan and larger treatment managed with financing when needed. That setup isn't right for everyone, but it often solves the exact gap that public aid and traditional insurance leave behind.

The least effective approach is usually waiting without a plan. Even if you don't schedule treatment today, call an office, ask for fees, ask whether they offer membership options, ask whether they work with CareCredit or Cherry, and ask what can be phased. People feel less overwhelmed once the choices are concrete.

A good affordability conversation should leave you with options, not pressure.

If your budget is extremely limited, a community clinic or public resource may have the lowest fees. If you need faster care, a private office that offers same-day evaluation, an in-house savings plan, or financing may be more practical. The most affordable option is the one that gets the problem addressed before it becomes more expensive.

In many cases, yes. A membership plan may reduce the office fee, and financing may help spread the remaining balance into monthly payments. Ask the office to explain the order clearly so you understand what is included and what amount, if any, would be financed.

Call a dental office and ask for an exam-focused visit, the fee range, and whether payment options are available. Don't wait until the pain becomes severe. Even if treatment needs to be phased, getting a diagnosis early gives you more choices.

That depends on the financing provider and the type of application process used. If you're trying to understand how collections, account reporting, or debt-related terms can affect your credit history, this plain-language Superior Credit Repair Capio Partners guide can help you understand the broader financial side before you sign anything.

If you're trying to sort through affordable dental care options for your family, Clayton Dental Studio is one local option for Humble and the greater Houston area. The office offers routine dental care, emergency visits, in-house savings plans, and financing options, which can help families compare practical ways to move forward without guessing about cost.